Cash-Pay Physical Therapy: Is It Worth It? A Breakdown of Costs and Value

Written by Connor Sheeks PT, DPT · Published May 2026 · Last reviewed May 2026

Reading time: approximately 8 minutes

If you have health insurance, paying out of pocket for physical therapy probably feels counterintuitive. You've been paying premiums for years. Why would you choose to pay again separately?

It's a fair question and it deserves a direct answer. The honest reality is that insurance-based PT and cash-pay PT are not the same product. They differ in ways that directly affect your outcomes: who treats you, for how long, with what level of individualization, and whether your care continues until you're actually better.

This article breaks down what cash-pay PT actually costs, what you're getting for that cost, how it compares to the real cost of insurance-based PT once you do the math, and how to decide which model is right for your situation. We'll include Spine33 Rehab's own pricing so there's nothing vague about it.

What you'll learn in this article

• Why insurance-based PT and cash-pay PT are structurally different products

• What cash-pay PT actually costs — including Spine33's pricing

• The real cost of insurance-based PT after deductibles, copays, and time

• A side-by-side comparison of both models

• The specific advantages of cash-pay care for spine conditions

• How HSA, FSA, and out-of-network benefits reduce your out-of-pocket cost

• How to decide which model makes sense for your situation

Why Insurance-Based PT and Cash-Pay PT Are Different Products

This is the part most people don't fully understand until they've been through the insurance system. The differences are not cosmetic; they affect clinical outcomes.

The insurance model creates structural incentives that work against you

Physical therapy clinics that accept insurance operate on a volume model. Insurance reimbursement rates have declined significantly over the past two decades while operating costs have risen. To remain profitable, clinics must see more patients per therapist per hour — often two to three patients simultaneously.

What this looks like in practice: your physical therapist greets you, assesses you for a couple of minutes, sets you up with a technician or aide for your exercise circuit, checks back briefly, and moves to the next patient. The hands-on, individualized time with a licensed PT may be fifteen to twenty minutes per visit. The rest is supervised exercise you could theoretically do at a gym.

This isn't a criticism of individual therapists. Many are excellent clinicians working within a system that limits what they can deliver. It's a structural problem created by how reimbursement works.

Insurance controls how long you're treated, not your therapist

Prior authorization, visit limits, and medical necessity reviews mean that your insurance company — not your physical therapist — often determines when your care ends. The average insurance-covered PT course is 6–12 visits. For chronic spine conditions, that is frequently not enough to produce durable outcomes.

Many patients are discharged when insurance stops covering, not when they've reached their functional goals. They may feel better than they did at the start but not as well as they could be. Months later they're back in pain, starting the cycle again.

Cash-pay removes those constraints

In a cash-pay model, your therapist works for you. There are no prior authorizations, no visit caps, no pressure to discharge you before you're ready. The relationship is direct: you and your provider, focused on your goals, for as long as it takes to reach them.

At Spine33 Rehab, every session is one-on-one for the full session duration. No aides. No shared time. No being set up on a machine while your therapist sees someone else.

What Cash-Pay PT Actually Costs

Cash-pay PT rates vary by provider, location, and specialization. National averages for private-pay PT range from $100 to $250 per session, with specialist practices and telehealth providers typically in the $125–$175 range.

Spine33 Rehab Pricing

Initial Evaluation (60 minutes): $175

Follow-up sessions (45 minutes): $99

Typical full course of care: 4-10 sessions

Estimated total investment: $571 - $1,165 for a complete course

All sessions are 1:1 with a licensed Doctor of Physical Therapy

HSA and FSA funds are accepted. Superbills provided for out-of-network reimbursement.

No contracts. No cancellation fees. No visit minimums.

These numbers are real and we're not going to obscure them. For many people, the question is whether that investment produces better value than what they'd get through insurance. To answer that honestly, you need to know the real cost of insurance-based PT.

The Real Cost of Insurance-Based PT

The sticker price of insurance PT looks lower, but the actual out-of-pocket cost is frequently higher than it appears, and the value delivered is often lower than expected.

Deductibles come first

The majority of insurance plans have annual deductibles ranging from $1,000 to $5,000 for individuals (higher for families) before coverage kicks in. If you start PT in January — or anytime before you've met your deductible — you're paying the full negotiated rate per session, which is typically $150–$300.

Many people discover this only when the bill arrives. They assumed a $40 copay and received a $200 invoice instead.

Copays add up across a full course

Once your deductible is met, you pay a copay per visit — typically $30–$80 depending on your plan. A full course of PT at 8 visits equals $240 – $640 in copays alone, after already having paid your deductible. For a $2,000 deductible plus $60 copays across 8 visits: your actual cost is $2,480. That's before accounting for premium payments.

The time cost is real

Insurance-based PT requires in-person attendance at a clinic. Travel time, scheduling around clinic hours, waiting rooms, and the administrative friction of dealing with authorizations and billing disputes all have real costs (in time and stress) that don't show up in the copay number.

Telehealth cash-pay PT eliminates all of that. Sessions happen from your home, on your schedule, with no commute and no waiting room. Same expertise.

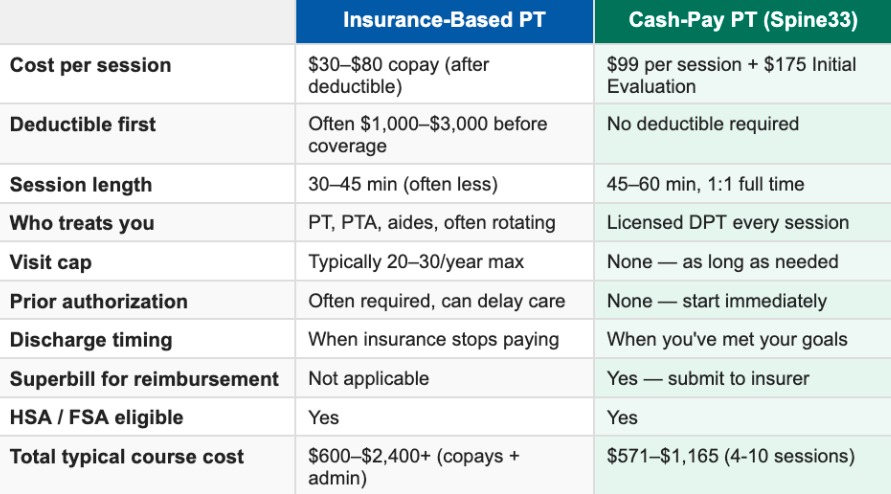

Side-by-Side: Insurance PT vs. Cash-Pay PT at Spine33 Rehab

The math is closer than most people expect. And when you factor in deductibles, visit quality, and the likelihood of actually reaching your goals, the value case for cash-pay becomes clearer.

The Specific Advantages of Cash-Pay for Spine Conditions

Spine rehabilitation specifically benefits from the cash-pay model for reasons beyond the general structural arguments above.

Chronic spine conditions need more time than insurance allows. Chronic low back pain, disc herniation, stenosis, and cervicogenic headache all respond to progressive, individualized rehabilitation over 8–16 weeks. With Spine33 Rehab, we give you the education and tools to rehabilitate in this timeline with less visits, all on your own or with messaging support. Follow-up visits are encouraged sparingly and when necessary. The average insurance-covered course rarely provides this. Cash-pay care also lets the program run as long as the evidence supports, not as long as the insurer approves.

Your home environment is clinically relevant. In telehealth PT, your therapist assesses your actual workstation, your actual movement patterns at home, and builds your program around your actual equipment. This context is not available in a clinic setting and directly improves program specificity.

Direct specialist access matters for complex presentations. Insurance clinics are generalist practices. Spine33 Rehab treats only spine conditions. The clinical depth that comes from seeing hundreds of patients with back pain, disc herniation, stenosis, and cervicogenic headache is not the same as a generalist who rotates between ankle sprains, shoulder repairs, and low back pain.

Consistent provider relationship improves outcomes. Research on therapeutic alliance (the relationship between patient and provider) consistently shows it predicts outcomes in musculoskeletal rehabilitation. Seeing the same clinician every session, who knows your history and your progress, produces better results than rotating through whoever is available.

How to Reduce Your Out-of-Pocket Cost

HSA and FSA accounts

Physical therapy is a qualified medical expense under IRS guidelines. If you have a Health Savings Account (HSA) or Flexible Spending Account (FSA), you can use those pre-tax funds to pay for cash-pay PT. Depending on your tax bracket, this effectively reduces your cost by 22–37%. A $1,500 course of care costs $975–$1,170 in after-tax dollars when paid through an HSA or FSA.

Out-of-network reimbursement

Many PPO and some POS insurance plans include out-of-network benefits — meaning they will reimburse a percentage of costs from providers outside their network, which includes cash-pay practices. Spine33 Rehab provides a superbill (an itemized receipt with the diagnosis and procedure codes your insurer needs) that you submit directly for reimbursement.

Reimbursement rates vary widely — typically 40–70% of the allowed amount after your out-of-network deductible. It's worth calling your insurer and asking specifically: "Does my plan have out-of-network PT benefits, and what is my out-of-network deductible?" Many patients are surprised to find meaningful reimbursement available.

HMO and Medicare plans

HMO plans and Medicare typically do not provide out-of-network reimbursement. If you have one of these plans, cash-pay PT is fully out of pocket. Whether it's worth it depends on your specific situation, goals, and what in-network options are available to you. That's worth an honest conversation, not a blanket recommendation.

Before your first session: questions to ask your insurer

1. Have I met my deductible for the year? If not, how much remains?

2. What is my copay for outpatient physical therapy?

3. Does my plan have out-of-network PT benefits?

4. What is my out-of-network deductible, and have I met it?

5. What percentage of out-of-network PT costs does my plan reimburse?

6. Is there an annual visit cap for PT?

These answers let you calculate your actual cost in both models and make an informed comparison.

Who Cash-Pay PT Is — and Isn't — the Right Fit For

Cash-pay PT is not the right choice for everyone. Here's an honest breakdown:

Cash-pay PT tends to be a strong fit if:

You have a high-deductible health plan and haven't met your deductible. Your effective cost at an in-network clinic may be the same or higher

You've been through insurance-based PT before without achieving your goals

You have a chronic or complex spine condition that needs more than 12 sessions

Your schedule makes clinic-based PT difficult — early morning, evening, or weekend availability matters

You want to work with a specialist, not a generalist

You have HSA or FSA funds available

You have out-of-network benefits that will partially reimburse your costs

Insurance-based PT may be the better choice if:

You have a low-deductible plan with low copays and have already met your deductible

Your condition is straightforward and likely to resolve in 4-6 sessions

You have an HMO or Medicare plan with no out-of-network benefits and limited financial flexibility

You have post-surgical rehab needs in the early phases that require hands-on wound care or specific equipment not available via telehealth

We will tell you at your discovery call if we think in-person or insurance-based care is more appropriate for your situation. The goal is to get you the right care.

Key Takeaways

• Insurance-based PT and cash-pay PT are structurally different products — the differences directly affect your clinical outcomes

• Insurance PT often involves shared therapist time, visit caps, and discharge driven by coverage limits rather than your goals

• Cash-pay PT at Spine33 Rehab costs $99 per session after a $175 Initial Evaluation; a full course of 4-10 sessions totals roughly $571–$1,165

• The real cost of insurance PT (after deductibles and copays) is often comparable to cash-pay, especially early in the year

• HSA and FSA funds reduce your effective cost by 22–37% depending on your tax bracket

• Out-of-network benefits (PPO plans) can provide 40–70% reimbursement. Always ask your insurer

• Cash-pay is a particularly strong fit for chronic spine conditions, high-deductible plans, and patients who have been through PT before without durable results

• Whether cash-pay is right for you depends on your specific insurance situation, condition, and goals. An honest conversation is worth more than a blanket recommendation

Frequently Asked Questions

Is cash-pay physical therapy more expensive than using insurance?

Not always — and often not when you do the full math. If you have a high-deductible health plan and haven't met your deductible, you're paying the full negotiated rate at an in-network clinic anyway — often $150–$300 per session. Cash-pay PT at $99 per session after an Initial Evaluation may actually cost less. Once you factor in copays across a full course of care, the total is frequently comparable. The quality of care and individualization you receive for that cost is typically higher in a cash-pay model.

Can I use my HSA or FSA for cash-pay physical therapy?

Yes. Physical therapy is a qualified medical expense under IRS guidelines, which means HSA and FSA funds can be used to pay for cash-pay PT sessions. This reduces your effective out-of-pocket cost by your marginal tax rate — typically 22–37% for most working adults. Spine33 Rehab can provide itemized receipts compatible with HSA and FSA reimbursement.

Does Spine33 accept insurance?

Spine33 Rehab is a cash-pay practice and does not bill insurance directly. However, we provide a superbill — an itemized receipt with diagnosis and procedure codes — that you can submit to your insurer for out-of-network reimbursement if your plan includes out-of-network PT benefits. We recommend calling your insurer before your first session to understand your out-of-network coverage.

What is a superbill and how does it work?

A superbill is an itemized medical receipt that includes the service date, provider information, diagnosis codes (ICD-10), and procedure codes (CPT) that insurance companies require to process a reimbursement claim. After each session at Spine33 Rehab, we provide a superbill you can submit directly to your insurer. If you have out-of-network PT benefits, your insurer will reimburse you directly — typically 40–70% of the allowed amount after your out-of-network deductible.

How many sessions will I need?

Most patients with chronic spine conditions at Spine33 Rehab complete a full course of care in 4-10 sessions over 6–12 weeks, followed by an independent home program. Simpler presentations may resolve in 4–6 sessions. More complex or long-standing conditions may require 12–16. We discuss a realistic estimate at your initial evaluation based on your specific presentation, and we don't add sessions that aren't clinically justified.

Is telehealth physical therapy covered by insurance?

Coverage for telehealth PT varies significantly by plan and state. Some insurers cover telehealth PT at the same rate as in-person; others have restricted coverage. Since Spine33 Rehab is a cash-pay practice, this is less directly relevant, but if you plan to submit for out-of-network reimbursement, it is worth asking your insurer specifically whether telehealth PT visits are eligible for out-of-network reimbursement under your plan.

Want to know exactly what care at Spine33 Rehab costs — and what you get for it?

Book a free 15-minute discovery call with us today. No commitment, no pressure — just an honest conversation about whether Spine33 Rehab is the right fit.

spine33rehab.com | Book Your Free Call

About the Author

Dr. Connor Sheeks PT, DPT is a licensed physical therapist and the founder of Spine 33 Rehab PLLC, a cash-pay telehealth physical therapy practice specializing in virtual spine rehabilitation. He holds a Doctor of Physical Therapy (DPT) degree and has clinical experience treating chronic low back pain, lumbar disc herniation and radiculopathy, cervicogenic headache, lumbar spinal stenosis, postural dysfunction, and many other spinal pathologies. Spine33 Rehab currently serves patients in Tennessee via telehealth and is actively pursuing licenses in other states.

References & Sources

American Physical Therapy Association. (2023). Physical Therapy Consumer Survey. apta.org

Jette DU, et al. (2009). Quality impairments exist in physical therapy documentation for Medicare patients. Physical Therapy. doi:10.2522/ptj.20080506

Fritz JM, et al. (2012). Is there a subgroup of patients with low back pain likely to benefit from mechanical traction? Spine. doi:10.1097/BRS.0b013e31822ef74b

IRS Publication 502. (2024). Medical and Dental Expenses. irs.gov/pub/irs-pdf/p502.pdf

Kaiser Family Foundation. (2024). Employer Health Benefits Survey. kff.org